Tron

-

Posts

831 -

Joined

-

Last visited

-

Days Won

3 -

Donations

114.92 USD -

Points

997,250 [ Donate ]

Content Type

Profiles

Forums

Gallery

Twitch

Running Commentary

Events

Store

Downloads

Everything posted by Tron

-

So sorry for your loss. Cobra was the guy that invited me in to join the clan. He will be greatly missed.

-

Happy birthday dood. Sent from my iPhone using Tapatalk

-

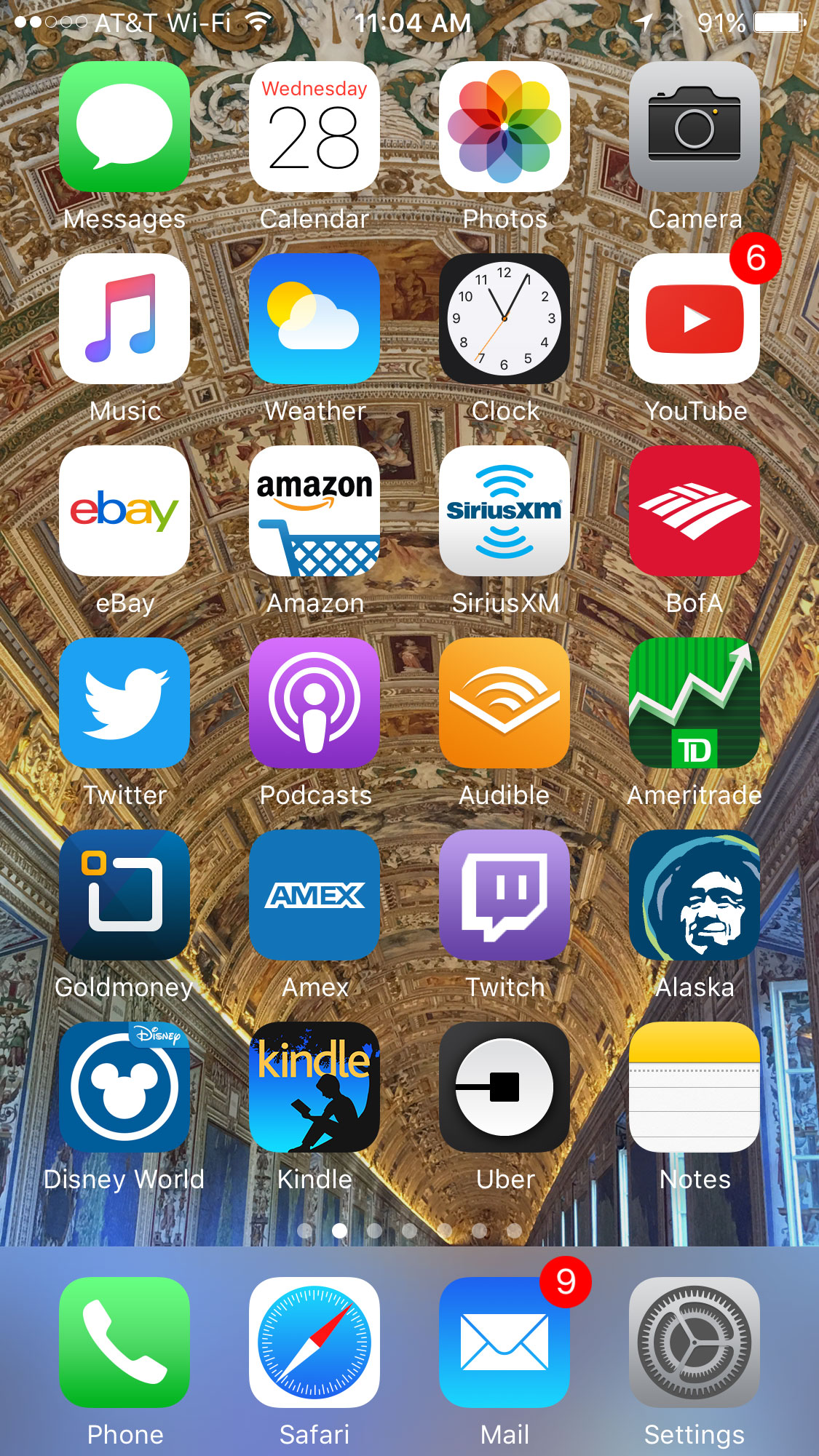

What apps are on your phone's home screen? Post a screen shot.

Tron replied to Tron's topic in General Discussion

How does a guy like you get away with using an app called "HipChat"? Also...kudos on the 200 unread emails...although my wife still has you beat, as the last time I looked at her phone she had 1327 unread next to the app icon. -

What apps are on your phone's home screen? Post a screen shot.

Tron replied to Tron's topic in General Discussion

You will now be inundated with requests for your Snapchat. -

Okay....interested to see what apps people have on the home screen of their phones as well as what they use for the background. I'm sure there have got to be some interesting choices out there.....and I'm sure a few of you will download a bunch of crazy ones just to make a picture to post here..but hell, that'll still be amusing. Here's mine...background is a picture I took of a ceiling in the longest hallway at the Vatican Museum in Rome.

-

Beginning to get pissed off

Tron replied to RobMc's topic in Call of Duty 4's Call Of Duty 4 Discussion

So how can we learn things like this?? I had no idea that RPG had DOUBLE the explosive radius of SMAW. Any othet tidbits like this we should know regarding explosive weapons? Sent from my iPhone using Tapatalk -

Dave Grohl also needs to be on the list. Sent from my iPhone using Tapatalk

-

Not sure about the best....but one of my all time favorites is someone that doesn't get nearly enough credit for his talent as a guitarist.....Vince Gill I saw him live about 20 years ago (sat in the front row) and I was mesmerized watching him play.

-

Happy B-Day 92 Protons

-

@Stricken The person that gets kicked when the servers are full and an XI member joins is only based on how many hours you have played in the last 30 days (I believe that's the time frame). So non-XI people who have not been playing very much over the last month will be the first kicked. It is fully automatic...not done by an Admin on the server.

-

@Nighto go fuck yourself.

-

Check this article out....it's a lot closer to becoming a reality than many people think: http://www.dailymail.co.uk/sciencetech/article-4602682/Robots-churn-400-burgers-hour-set-over.html

-

Nearly all fast food workers will be displaced by robotic technology eventually..but at a $25 an hour minimum wage, companies would be massively incentivized to invest in automation very quickly. Robots never call in sick, show up to work high or demand to have the day off so they can go participate in some nonsensical protest. Sent from my iPhone using Tapatalk

-

Just looked at the different starter packs...Can't decide between the War Pack for $5k or the Wing Commander for $10k lol

-

Cool...thanks for all the info. I'll definitely be on the lookout for the next time you are streaming on Twitch.

-

I click buttons while in my TD Ameritrade account...and then occasionally transfer some money into my checking account.

-

@FLDMARSHAL I presume you play Star Citizen? I heard about it at Pax Prime a couple years ago but have never tried it. What are your thoughts on it? Does it have a very steep learning curve until you are able to enjoy playing? Thanks...

-

@@Sammy I also just had a strange thing happen yesterday. I was the last person left on my team and there was only one person left on the other team. He went in and started an airstrike...and right after he came out of the animation for doing his airstrike..I killed him ending the round. The screen froze like usual showing we had won the round....and everything seemed fine...then his airstrike started...which I have seen happen before as well...having the bombs rain down after the round ended...only this time...it actually killed me....after I was in the frozen end of round screen. Not sure it has anything to do with what Chile was talking about in his case but thought I would let you know.

-

HAPPY BIRTHDAY!!!

-

Post pics of your lets see what people look like

Tron replied to Stringer's topic in General Discussion

Wait....you were on Charlie's Angels?? Lovely [emoji7] Sent from my iPhone using Tapatalk -

-

-

Perhaps the rejection of FOIA requests are related to the fact that minors are involved? Wouldn't surprise me at all that there are built in protections related to minors. This is also the case whenever minors are involved in criminal prosecution...they never release the names involved. Perhaps you should send an email to Judicial Watch...they are usually good at using litigation to force compliance with FOIA requests....just ask Hillary Clinton. As far as using this to confiscate firearms...The fact is that it just is not going to happen. There are hundreds of millions of firearms in the hands of private citizens. Physical confiscation would literally require doing a forced entry house to house search, and I can guarantee you that the day that starts to happen is the day that American Civil War 2.0 kicks off. I for one will NEVER voluntarily surrender my firearms regardless of what draconian laws are passed. As Leonidis once said...they can "come and take them" if they would like to try.

-

Still seems highly unlikely such a grand hoax would be committed like this. Where did these children who were killed ( but apparently not really killed) go?? Were they placed in the Federal witness protection program? Really? It would seem that it wouldn't be too difficult to actually track down one of those "dead" kids who were supposedly singing at the Superbowl and get an interview on camera. What would be the motivation of the individual families to participate in such a heinous hoax on society? You can't tell me that every single family that would be approached to participate in such a hoax would also be an anti-gun leftist douchebag. Surely at least one famkly would have been approached to participate and decided to come forward to report such a conspiracy because they disagreed with such a plan? Again, I 100% believe our government has been a perpetrator of evil acts on par with what this would be if it were a hoax. But the question one always must ask is "cui bono?" , or who stands to benefit? There simply is not enough "benefit" to go around to explain why so many families would go along with it.

-

I don't"blindly reject" the possibility that something like that could happen here. There is no doubt our FedGov has definitely been involved in false flags and other criminal activity. Just read the book "Legacy of Ashes" and you will realize how corrupt the CIA is. My points were simply based on the circumstances and highly dubious probability that Sandy Hook was some kind of grand "false flag" hoax where no children actually died. The evidence does not support such a hypothesis. Are there screwy details surrounding the post-shooting investigation and evidence...ok sure maybe there are. But given the sheer number of people that were there that day...I say pulling off such a hoax is literally impossible to do without evidence it was a hoax eventually surfacing. Sent from my iPhone using Tapatalk